What Every Bay Area Homeowner Needs to Know About Home Insurance

A practical guide to protecting your most significant financial asset

Why Home Insurance Is Non-Negotiable

For most people, their home is the most significant financial asset they will ever own. Mortgage lenders universally require it — but beyond the lender requirement, home insurance is the financial backstop that protects everything you have built. A single uninsured loss event can be catastrophic. The question is not whether to have it, but whether you have the right coverage.

What Home Insurance Actually Covers

A standard homeowners policy (HO-3) has several components that work together. The HO-3 is an industry-standardized policy form used by most insurers for single family homes — when you hear "standard homeowners policy," this is what that means:

- Dwelling coverage — rebuilds the physical structure if destroyed by a covered peril

- Personal property — replaces your contents

- Liability protection — covers you if someone is injured on your property

- Additional living expenses — pays for temporary housing if your home becomes uninhabitable

Replacement cost versus actual cash value is one of the most consequential decisions you will make. Actual cash value (ACV) pays what your property is worth today after depreciation — that is, its original value minus wear and tear over time, without any adjustment for how much prices have risen since it was new. For example, a 15-year-old roof that cost $30,000 to install may have depreciated to an ACV of $12,000. If it is destroyed, that is all you receive — even if the same roof costs $45,000 to replace at today's labor and material prices. ACV leaves you exposed on both ends: the age of the item and the inflation in replacement costs since it was originally installed. Replacement cost coverage pays what it actually costs to rebuild or replace at today's prices, regardless of the age or condition of what was lost — in the same example, the full cost to put a new roof on at current rates. Given Bay Area construction costs, the gap between ACV and replacement cost is routinely enormous. Most homeowners are significantly underinsured because their coverage was set at purchase and never updated to reflect rising costs.

Single Family Home vs. HOA / Condo: A Different Animal

Owning a condo or townhome within an HOA means you are operating in a split-insurance environment. The HOA carries a master policy that covers the building exterior, roof, common areas, hallways, and shared infrastructure — all funded in part through your HOA dues. Your personal responsibility is everything within your walls: interior fixtures, flooring, appliances, personal property, and your own liability. The standardized policy form for this is the HO-6, the condo/townhome equivalent of the HO-3. The critical step is reading the HOA's master policy before you buy to understand exactly where their coverage ends and yours must begin. Key gaps often include loss assessment coverage — your share of a loss that exceeds the association's policy limits — which is an exposure most condo owners don't discover until they receive an unexpected bill. Never assume the HOA has you fully covered.

The Bay Area's Unique Risk Landscape

Where you live in the Bay Area determines what coverage you need beyond a standard policy:

- Wildfire — Oakland hills, Los Gatos, Saratoga, Woodside, Portola Valley, Los Altos Hills, and any property in or near the Wildland Urban Interface (WUI) face elevated wildfire risk. Standard policies increasingly exclude or limit wildfire coverage in these areas.

- Flood — Standard policies never cover flooding. Low-lying communities with proximity to the bay or creek corridors — East Palo Alto, parts of San Jose, portions of Marin — require separate flood insurance through the National Flood Insurance Program (NFIP), a federally backed program administered by FEMA (the Federal Emergency Management Agency), or through private carriers. FEMA flood zone designation, shown on official Flood Insurance Rate Maps, determines both whether coverage is required and what it costs.

- Earthquake — Standard home insurance does not cover earthquake damage anywhere in California. The Hayward Fault and San Andreas Fault put virtually the entire Bay Area at meaningful risk. A separate earthquake policy — through the California Earthquake Authority (CEA) or private carriers — is the only way to protect against this exposure. Given the Bay Area's seismic history, this is a coverage gap that deserves serious consideration by every homeowner in the region.

The California Insurance Crisis

California's insurance market has undergone a fundamental disruption. Catastrophic wildfire losses — the 2017 Wine Country fires, the 2018 Camp Fire, and the 2025 Los Angeles fires — produced insured losses that far exceeded what carriers had priced into their models. The response has been dramatic: State Farm, Allstate, and several other major insurers have stopped writing new policies in California or exited the state entirely. Those that remain have raised rates aggressively — average homeowners premiums in California increased by more than 30% between 2020 and 2024, with high-risk wildfire zones seeing increases of 50% or more, and some insurers filing for increases exceeding 20% in a single year. For homeowners in those areas, finding standard market coverage at any price has become genuinely difficult.

The California FAIR Plan: Insurer of Last Resort

When standard market coverage is unavailable, the California FAIR Plan provides basic fire insurance as a backstop. It is not a comprehensive homeowners policy — it covers fire, smoke, wind, and a limited set of perils, but excludes liability, theft, and many other standard coverages. Premiums are typically higher than standard market policies, and coverage limits may be insufficient for higher-value properties. Homeowners relying on the FAIR Plan generally supplement it with a separate "Difference in Conditions" (DIC) policy to fill the gaps.

What Can Make a Property Difficult or Impossible to Insure

Underwriters evaluate risk at the property level. Factors that commonly trigger coverage denial or very high premiums include:

- Roof age and material — old shingle roofs or wood shake roofs are significant red flags

- Knob and tube wiring or other outdated electrical systems

- Galvanized plumbing past its useful life

- Location in a high fire hazard severity zone (HFHSZ) as designated by CAL FIRE

- Prior claims history on the property

- Deferred maintenance indicating elevated loss risk

For buyers, a pre-purchase insurance consultation can identify these issues before you are contractually committed.

The broader market crisis has made this more consequential for existing homeowners, not just buyers. With so many large insurers having exited California, those that remain are in a position to be selective — and they are. Insurers are actively reviewing their existing books of business and non-renewing policies on properties that present elevated risk. A homeowner who receives notice that their policy will not be renewed because of an aging roof, outdated wiring, or old plumbing may find that replacement coverage is difficult or expensive to obtain. If your home has any of these characteristics, addressing them proactively is both a risk management decision and an insurance strategy.

A practical maintenance note: every homeowner should conduct an annual review of their coverage with their insurer or broker. Construction costs, home values, and personal property all change over time, and a policy that was adequate at purchase may leave you significantly underinsured today. An annual check takes an hour and can prevent a much more painful discovery at the time of a claim.

Brokers, Agents, Bundling, and Major Carriers

Independent brokers can shop your risk across multiple carriers — a significant advantage in a constrained market. Captive agents represent a single insurer only. In California's current environment, the ability to access the broader market is particularly valuable.

Major insurers still active in California include State Farm, Farmers, CSAA (AAA), Travelers, Chubb, and AIG for higher-value properties. Availability varies significantly by location and risk profile.

Bundling home, auto, and umbrella policies with a single carrier typically produces meaningful discounts — often 10–25%. However, in a hard market where your best home insurance option may be a specialty or non-standard carrier, bundling may not always be possible or optimal. Weigh the discount against the quality of coverage.

When to Start: During Contingencies, Not After

The right time to investigate home insurance is during your contingency period, before you are committed to the purchase. Discovering that a property is uninsurable — or only insurable through the FAIR Plan at a high premium — after you have removed contingencies puts you in a very difficult position. Treat insurability as part of your due diligence, not an afterthought. Your lender will require a binder before closing anyway — start the process early enough that you have real options if the first answer is no.

Questions about insurance as part of your home purchase? Reach out — navigating these decisions is part of what I do.

Appendix: Bay Area Risk Maps

The maps below illustrate the three primary risk exposures Bay Area homeowners should factor into their insurance planning: wildfire, flood, and earthquake. Each represents a hazard that a standard HO-3 homeowners policy does not cover and requires a separate policy to address.

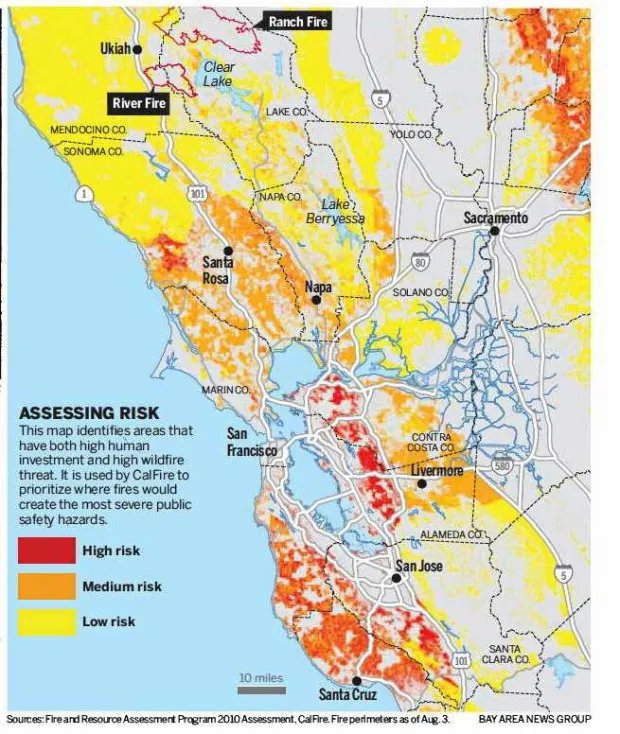

A.1 Wildfire Risk Zones

Source: CAL FIRE / Fire and Resource Assessment Program (FRAP). Red areas denote high risk, orange medium risk, yellow low risk. Properties in red and orange zones face the greatest challenges obtaining standard market insurance coverage and are most likely to require FAIR Plan or specialty carrier policies.

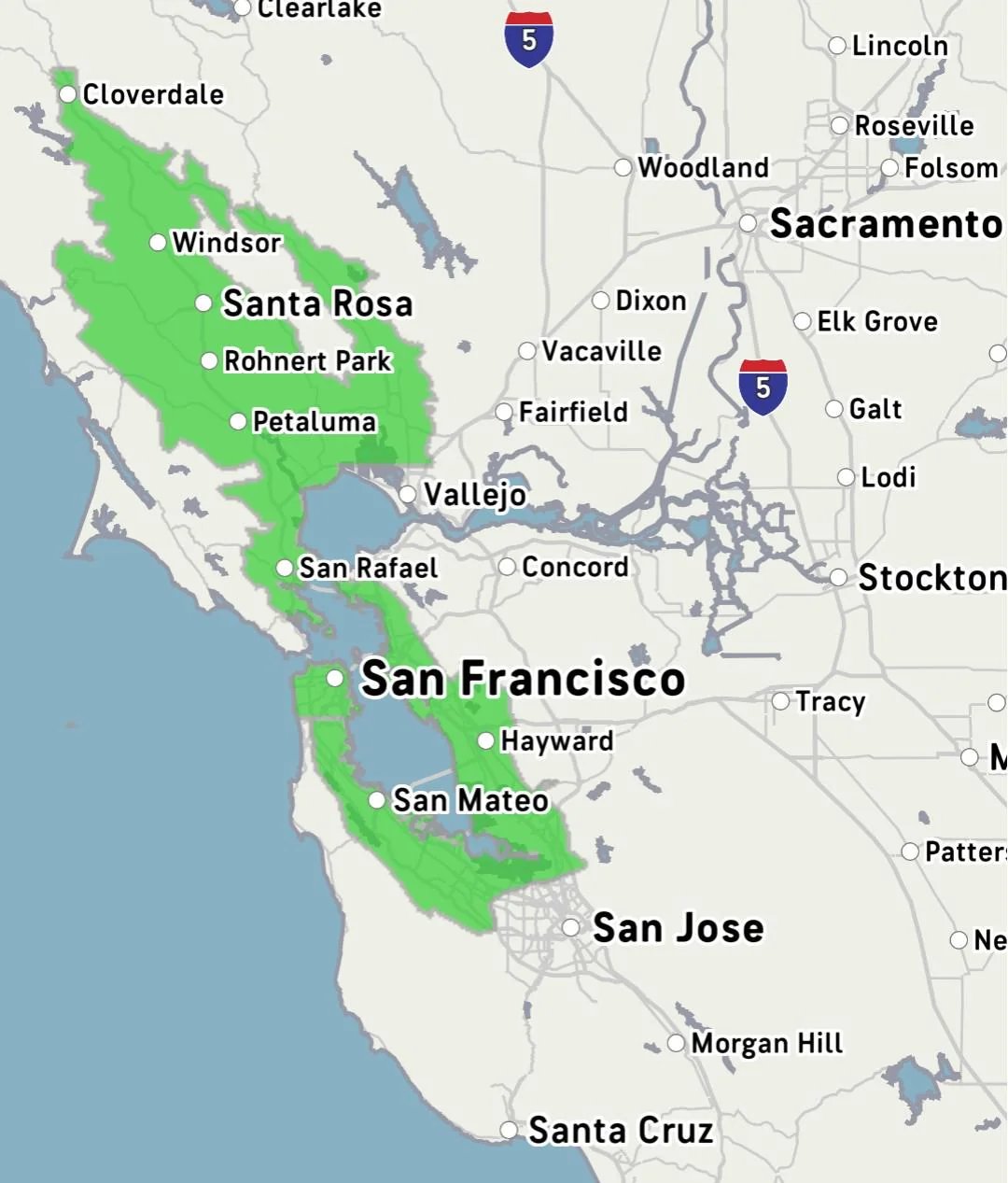

A.2 Flood Risk Zones

Source: FEMA / Risk Factor. Green areas indicate elevated flood exposure — communities in or near these zones are most likely to be in FEMA-designated Special Flood Hazard Areas requiring separate flood insurance. Properties with federally backed mortgages in these zones are legally required to carry flood coverage.

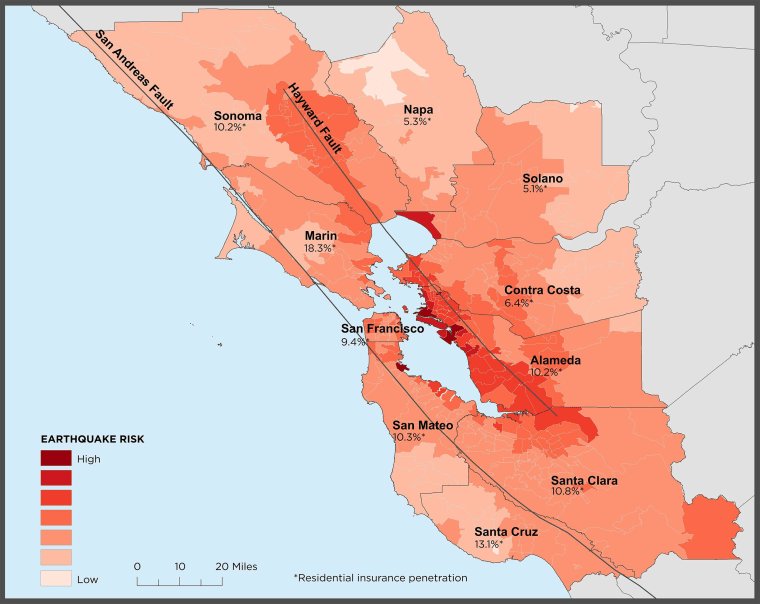

A.3 Earthquake Risk Zones

Source: California Earthquake Authority / USGS. Darker red areas indicate highest seismic risk, concentrated along the Hayward and San Andreas fault corridors. Percentages shown per county reflect residential earthquake insurance penetration rates — notably low across the region, underscoring how underprotected most Bay Area homeowners are against this risk.